According to a new report from Smithers Pira, the Offset to digital transition is accelerating: in 2020 digital will be 17.4% of value and 3.4% of all print and printed packaging volume.

The Future of Digital versus Offset Printing to 2020provides in-depth analysis of the main technology trends and the key issues affecting the digital and analogue printing markets. provides in-depth analysis of the main technology trends and the key issues affecting the digital and Offset printing markets. Digital is growing because it can offer advantages that offset print cannot provide. As colour digital presses came to market the initial drivers were for low cost, short runs and quick turnaround. As more companies used the technology, new applications and business models developed for print-on-demand and short-run books. There is increasing demand for photobooks and photo products, where digital print linked to online ordering has enabled a multi-billion dollar market to flourish.

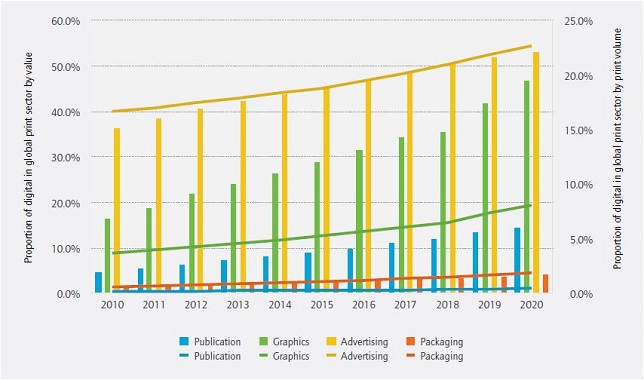

The penetration of digital varies across particular market sectors. Advertising print and graphics have a higher proportion of digital print in the overall mix than for packaging and publishing where books are taking off and there is some newspaper inkjet printing. The varying take up is summarised in Figure 1.

FIGURE 1 Digital print penetration into the global print market by application 2010–20 ($, constant values and volume in A4 prints)

Digital print can incorporate variability that makes it more effective than the static alternative. Users of digital print are innovating applications, and exploring new ways to offer novel functions and features to print buyers that are valued and sell at a premium. Smithers Pira ran a market research programme in June-July 2015 to determine the status and to identify the key drivers and barriers to the adoption of digital printing. The continuing increase in shorter run lengths was identified as the most important issue; with the improvements in technology ranked second, equal with the low setup costs; while environmental benefits scored lowest.

Printing technology is continuing to develop for analogue processes, but the major developments are taking place in digital printing – and particularly inkjet, which is enjoying major investments in R&D on heads, inks, and printing systems.

The choice between digital and analogue is not always an either-or decision. As many print suppliers employ both offset and digital as part of their production capacity the two technologies can be complementary. There is greater flexibility for planners to put short runs and quick turnaround on the digital presses, with longer runs on the offset equipment. This can improve the overall efficiency of the print shop greatly. End-use customer preferences and demands are changing and fragmenting. Having both digital and offset solutions means a company can offer the most appropriate solution to the customer.

Digital printing will continue to grow in most print sectors across the world. Mono webfed electrophotography is being superseded by full-colour inkjet; but despite this drop, the volume and value of electrophotography will continue to rise as colour applications grow. Innovative users will find more applications and niches to exploit the advantages of digital and, although some may be at the expense of analogue printing, they will also open up totally new opportunities.

Print the page

Print the page